Italy (and Europe): the problem isn't housing. It's incomes that no longer hold up and a market that has become too concentrated.

An analysis of 22 million listings across Europe reveals a structural crisis: the issue isn’t price, but the relationship between housing and income

Original Italian article by ‘Esco quando voglio’👇

One of those reports has just come out — the kind that is actually worth reading, not just quoting.

The European project HOUSE4ALL, developed within the ESPON research framework, analysed around 22 million property listings across Europe, cross-referencing them with average disposable income at municipal level. Not national averages, not perceptions: granular data, territory by territory, finally allowing us to understand how sustainable it really is to live in a given place.

In Italy, the analysis was published and brilliantly covered by Il Sole 24 Ore in its Lab24 section.

The result, in short, is quite clear.

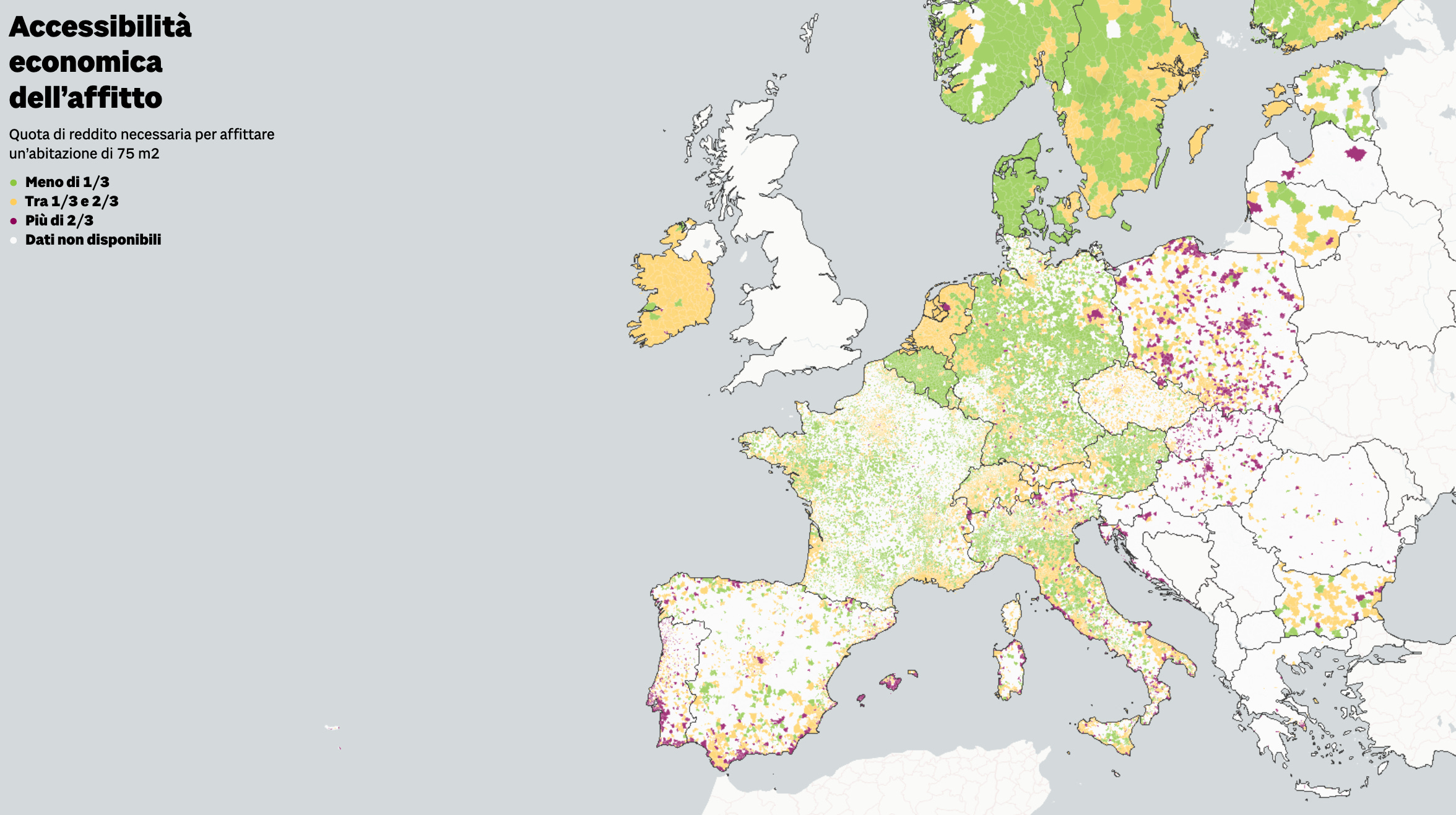

Across much of Europe, a significant share of the population lives in municipalities where, to access a standard home, it is necessary to allocate well over one third of their income — the commonly accepted threshold for affordability. In many cases it reaches half, in others it exceeds it.

In this context, Italy — often portrayed as a particularly problematic case — actually fits into a much broader dynamic. With clear critical issues, of course, but also with specific characteristics that make the picture less obvious than we might think.

And it is precisely when you go into the detail, municipality by municipality, that the most interesting insights emerge.

In Italy, we always start from the same assumption: that we are worse off than others. That our market is more distorted, more fragile, more complicated. A mix of tourism pressure, rent-seeking, bureaucracy and stagnant wages that inevitably makes everything harder.

Then the real data arrives. The data on affordability, on the actual sustainability of housing costs.

And the picture, in some ways, shifts — much like what happens when short-term rentals are discussed superficially.

Because affordability does not mean whether a house is expensive or cheap in absolute terms. It has nothing to do with price alone. It means something far more concrete, and if we’re honest, more uncomfortable: how much that house weighs against the income of the people who live there.

It is a relationship, not a number.

And it is this relationship that overturns many assumptions.

Take an apparently simple example: Cortina d’Ampezzo. Extremely high prices, among the highest in Italy. In common narratives, a completely inaccessible place. And yet, if you look at the relationship between prices and the incomes of those who actually buy and live in that market, the situation is less extreme than it appears. Not because houses are cheap — clearly they are not — but because the market aligns with a very high income bracket.

On the other hand, regions like Tuscany — often perceived as “mid-range” — show much more problematic dynamics. Strong prices, driven by international and tourist demand, but local incomes that simply do not keep up. And that is where affordability truly breaks down.

When you move to the numbers, the fracture becomes clear.

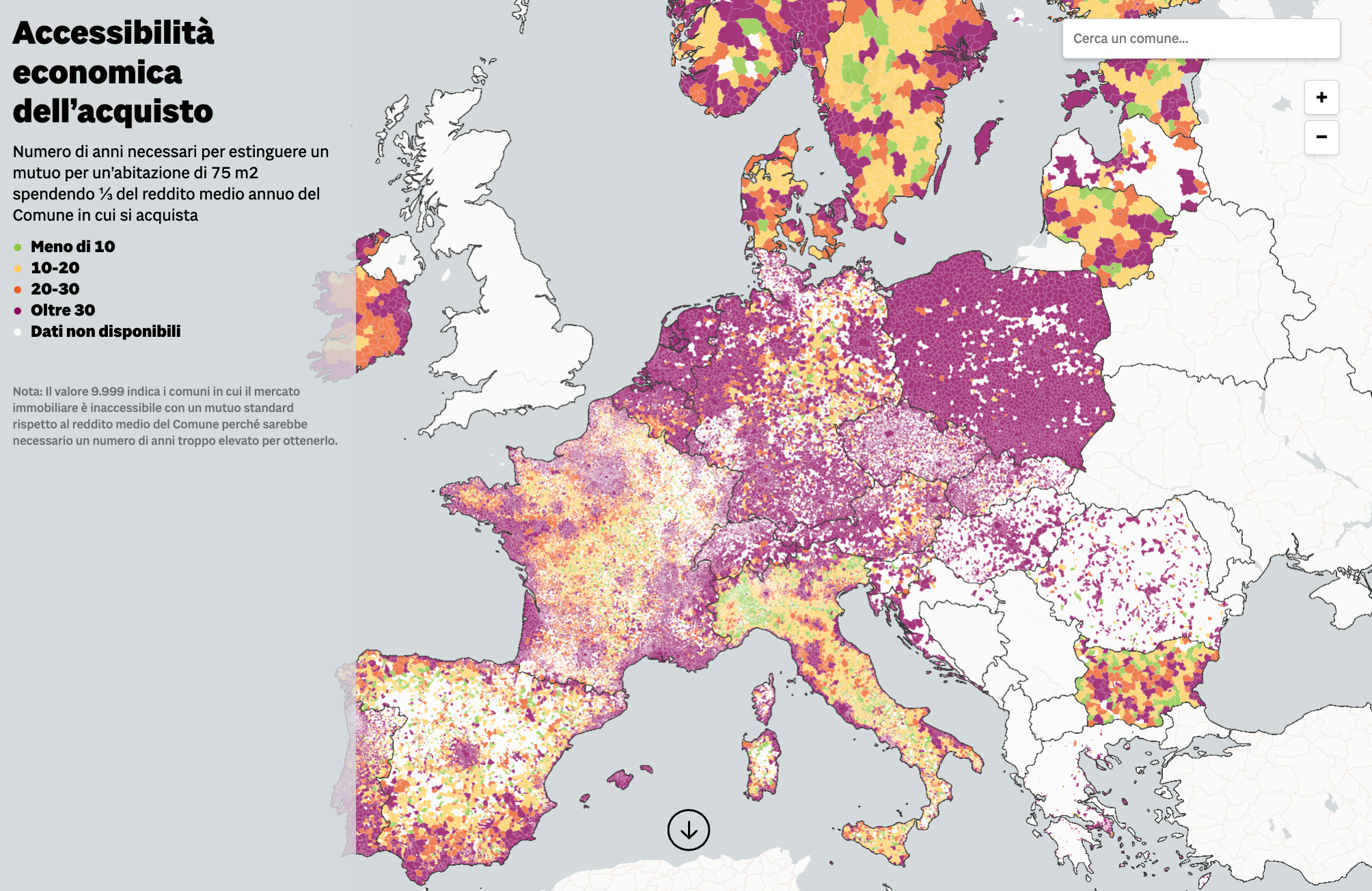

In the HOUSE4ALL model, a home is considered affordable when the cost of rent or mortgage does not exceed one third of disposable income. This is a widely accepted benchmark. Beyond that, you enter a zone of tension. Far beyond it, a zone of unsustainability.

And in Europe, a large portion of the population lives in municipalities where this threshold is exceeded — often by a wide margin.

In Italy, the data is quite explicit.

To rent a standard 75 sqm home:

in Naples, it requires about 73% of average income

in Florence, 66%

in Venice, 60%

in Rome, 56%

in Milan, 52%

These are not just signs of difficulty. They describe a system that is no longer sustainable in its traditional form.

And this is not only about major cities.

In fact, one of the most interesting aspects of the study is that the most extreme imbalances are often found elsewhere: in tourist areas, coastal regions, and places where external demand — whether tourism-driven or international — has pushed prices far beyond the economic capacity of local populations.

The case of Santa Maria del Cedro, in Calabria, is striking: renting a standard home would require more than double the local average income. In Dorgali, Sardinia, it reaches around 169%. In mountain areas, Borca di Cadore exceeds 118%, while Valfurva reaches 116%.

Here, the issue is not the housing market itself. It is the misalignment between two worlds: those who arrive, and those who stay.

Then there is the other side of the story — often overlooked.

Inner areas. Small municipalities. The territories we have been describing for years as fragile, depopulating, marginal.

If you look at affordability indexes, many of these places are among the most accessible.

Not because they function better, but because prices are extremely low and market pressure is limited.

It is an interesting, but also ambiguous, finding.

Because these places are accessible on paper, but often not in real economic terms. Incomes are low, opportunities limited, services reduced. So yes, housing is cheap — but that does not automatically mean it is truly affordable in the full sense of the term, meaning sustainable within a long-term life project.

And this opens up a broader reflection.

The European housing crisis is no longer just an urban issue. It is not only about large cities or capital regions. It is a systemic crisis of the relationship between housing, income, and social mobility.

And this becomes even clearer when looking at home ownership.

According to the data, in many Italian cities it would take over 30 years of mortgage payments — assuming one third of income — to purchase a standard home. In some cases, the numbers become almost absurd. In Salerno, for example, estimates reach nearly 120 years. In Sesto San Giovanni, around 70 years. Among regional capitals, Trento approaches 80 years, while Venice, Rome, and Bologna range between 55 and 63 years.

In other cases, such as Florence and Naples, the market is so disconnected from incomes that purchasing with a standard mortgage is simply no longer considered feasible.

On top of this, there is another often underestimated factor: the initial deposit. In Northern Italy, figures range between €40,000 and €50,000, in line with markets such as southern Germany or Northern European cities. A barrier that excludes a growing share of the population — especially younger people — and inevitably shifts pressure onto the rental market.

The outcome is visible, even if we don’t always read it this way.

We are moving towards a model where more and more people will remain renters for longer. Possibly for life. And in a country like Italy — historically built around home ownership — this is not a minor shift. It is structural.

So perhaps the question is no longer where housing is cheaper.

But where there is still a balance between cost of living, income, and quality of context.

And today, that balance is rarely found where everyone is looking.

It is found just outside.

Just outside Lecce, for example, a 10-kilometre difference is enough to move from rents approaching or exceeding €700–800 to solutions between €300 and €400. Not a different region, not a different market — the same territory, under very different pressure.

In parts of the Maremma, about an hour from Siena, you can still find homes between €500 and €600, in contexts where the relationship between space, quality of life, and cost begins to make sense again. And dozens of similar examples could be found across the country.

These are not isolated cases. They are patterns.

These are the territories where, in addition to being more accessible, there is another often overlooked factor: a vast supply of housing. Empty homes, underused properties, abandoned assets. Not because they are unnecessary, but because for years no sustainable model has been found to bring them back into use.

And this is where the conversation changes completely.

Because not every house needs to be sold.

And not every property needs to end up in short-term rentals.

In many of these places, it makes far more sense to focus on transitional or mid-to-long-term rentals — responding to a real demand: people relocating, working remotely, testing new territories — and, importantly, often proving simpler to manage and more profitable over time than a compressed three- or four-month seasonal cycle.

The paradox is clear.

We have territories full of houses and empty of services.

And others full of demand and completely saturated.

And we keep treating them as if they were the same market.

It is exactly in this gap that a real opportunity emerges.

And that is where we have chosen to work for some time now.

With ITS ITALY, we don’t just observe these territories: we invest in them, develop projects, and try to build housing and hospitality models that make sense over time. And through ITS Journal, we aim to tell their real story every day, beyond simplifications.

Not as cheap shortcuts.

Not as “low-cost opportunities”.

But as places where, if work, services and accessibility are reconnected, the relationship between life and housing cost can start to make sense again.

Because in the end, the question is not how to find a cheaper house.

It is how to live better, spending the right amount relative to what you earn.

And today, paradoxically, that is more likely to happen outside the radar than within it.